For the better part of the last decade, multifamily has been the default allocation for real estate investors. It offered perceived stability, strong demand, and relatively predictable income.

That assumption is being tested.

Supply dynamics have shifted. Capital costs have changed. And the gap between projected performance and realized outcomes has widened in several markets.

At the same time, a less visible segment of the market – small-bay industrial – has continued to demonstrate resilience.

The difference is not cyclical alone. It is structural.

Capital is not just chasing yield. It is repositioning around durability.

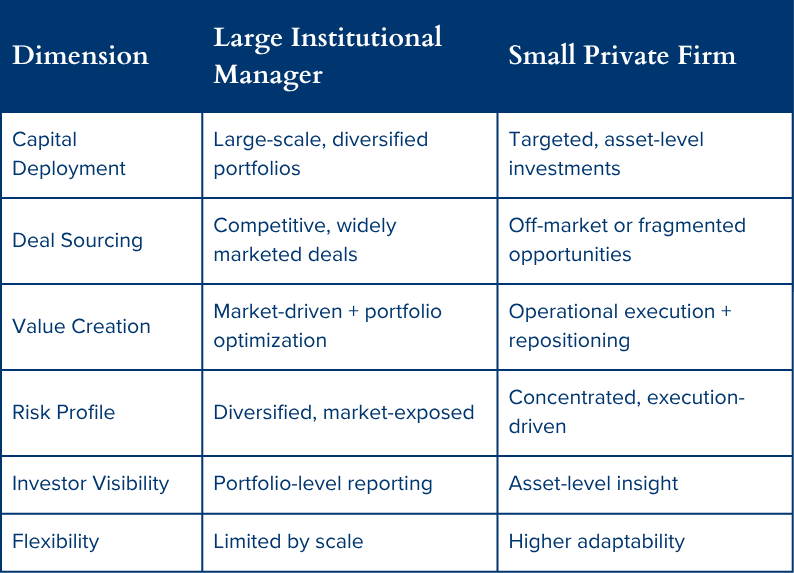

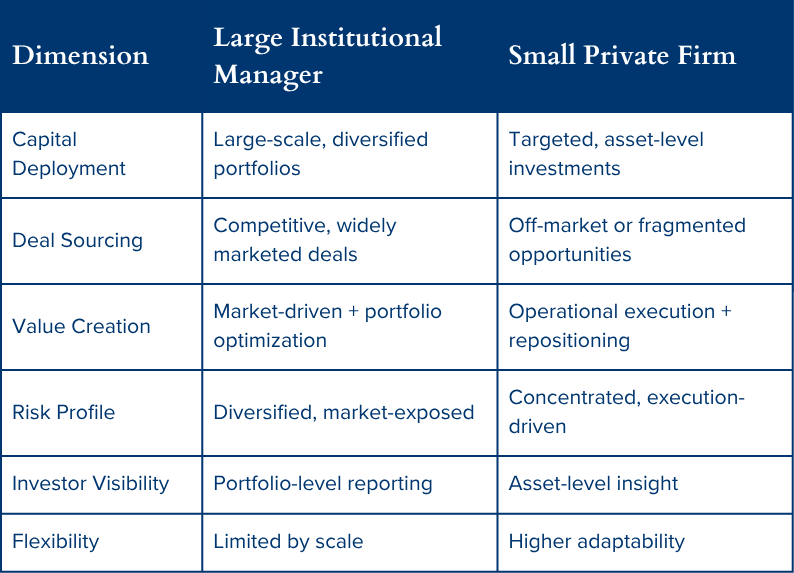

Why Multifamily Became the Default

Multifamily earned its position through a combination of demand fundamentals and institutional accessibility.

Population growth, urbanization, and household formation supported long-term demand. Lease terms were short, allowing rents to reset frequently. Large-scale assets enabled institutional capital to deploy efficiently.

For a period, these characteristics aligned.

However, the same features that supported growth can introduce pressure when supply expands and affordability tightens.

Structure matters in both directions.

Where Multifamily Is Facing Pressure

Recent data reflects a meaningful shift in multifamily fundamentals across several U.S. markets.

In 2025 and into early 2026, multifamily vacancy rates in high-growth Sunbelt markets have moved into the 7% to 9% range, driven largely by new supply deliveries. In most submarkets, rent growth has flattened or declined as operators compete for tenants.

Supply is the primary driver.

Development pipelines that were initiated during periods of low interest rates are now delivering into a different capital environment. Increased operating costs, higher insurance premiums, and affordability constraints have added additional pressure on net operating income.

Short lease terms, once viewed as an advantage, now accelerate exposure to market softness.

Income adjusts quickly. Not always upward.

Why Small-Bay Industrial Is Structurally Different

Small-bay industrial operates under a different set of constraints.

These assets typically consist of multi-tenant buildings with units ranging from approximately 1,000 to 25,000 square feet. They serve a fragmented tenant base that includes local service providers, light manufacturers, contractors, and last-mile distributors.

Demand is local. Supply is constrained.

Recent market data continues to show that small-bay vacancy remains consistently below broader industrial averages, often in the 2% to 5% range in infill markets, even as larger warehouse vacancy has expanded.

The reason is straightforward.

Small-bay products are difficult to develop at scale. Zoning constraints, land scarcity, and redevelopment pressures limit new supply. At the same time, demand remains stable because tenants rely on proximity to customers and labor.

Scarcity compounds value.

Supply Dynamics Drive Pricing Power

The divergence between multifamily and small-bay industrial begins with supply.

Multifamily supply can be scaled relatively quickly when capital is available. Large projects deliver hundreds of units at once, increasing inventory in concentrated submarkets.

Small-bay industrial does not scale the same way.

Projects are typically smaller, more fragmented, and often constrained by infill land availability. In many cases, existing inventory is being repurposed or redeveloped into other uses, further reducing supply.

This creates a persistent imbalance.

When supply is limited and demand is steady, pricing power shifts to the landlord. That dynamic has supported continued rent growth in many small-bay industrial submarkets, even as other asset classes normalize.

Tenant Structure and Income Stability

Tenant composition introduces another key difference.

Multifamily assets rely on a large number of individual tenants with relatively short lease durations. Turnover is frequent. Income resets annually.

This creates flexibility, but also volatility.

Small-bay industrial properties typically house 10 to 100 tenants across diverse industries. Lease terms are often longer, and tenants tend to remain in place due to location dependence and relocation costs.

Diversification reduces concentration risk. Businesses don’t move for a new job they stay put like the occupants of apartments move as their careers change.

If a single tenant vacates a multifamily unit, the impact is minimal. However, when broader market conditions weaken, occupancy and rent levels can shift across the entire asset simultaneously.

In contrast, small-bay industrial income is distributed across multiple businesses, industries, and lease schedules. This creates a more staggered and resilient income profile.

Income durability matters more than growth projections.

Value Creation: Operational vs Market-Driven

Value creation mechanisms also differ meaningfully between the two asset classes.

In multifamily, rents are typically closer to market at acquisition. Value creation often depends on continued market growth, operational efficiencies, or capital improvements.

In small-bay industrial, below-market rents are more common, particularly in assets owned by long-term operators.

This creates embedded upside.

As leases roll, rents can be reset to market levels. Modest capital improvements, such as exterior upgrades or unit enhancements, can support higher tenant retention and pricing.

Operational execution becomes the primary driver of value.

This distinction is important.

Market-driven appreciation can reverse. Operationally driven income growth is more controllable.

A Practical Example of Industrial Value Creation

Hanson Capital’s recent Phoenix industrial portfolio sale illustrates how these dynamics translate into results.

Across an eight-asset portfolio, the firm aggregated and repositioned small-bay industrial properties acquired between 2020 and 2021. Through lease optimization, tenant alignment, and operational improvements, the portfolio was stabilized and sold to a buyer group backed by J.P. Morgan.

The second tranche alone converted $9 million of equity into $43 million of proceeds, producing a 4.0x equity multiple and 35.4% IRR.

Individual assets reflected similar patterns.

A 65,000-square-foot property acquired for $3.7 million was sold for $10.5 million after repositioning and lease stabilization. Another asset acquired for $2.8 million was sold for $8.4 million following similar operational improvements.

These outcomes were not driven solely by market expansion.

They were the result of structured execution applied over time.

What This Means for Capital Allocation

The comparison between multifamily and small-bay industrial is not about one asset class replacing another.

It is about understanding how each behaves under current conditions.

Multifamily continues to offer scale and liquidity. However, it is more exposed to supply cycles, affordability constraints, and operating cost pressures.

Small-bay industrial offers a different profile:

- Supply-constrained in infill markets

- Diversified tenant base

- Longer lease structures

- Operational value creation opportunities

These characteristics have increasingly attracted institutional attention.

Capital is moving toward durability.

That does not eliminate risk. It changes how risk is distributed and managed.

Executive FAQs

Is small-bay industrial safer than multifamily?

No asset class is inherently risk-free. However, small-bay industrial often benefits from tenant diversification, supply constraints, and more stable income structures, which can reduce volatility in certain market conditions.

Why is multifamily experiencing pressure in some markets?

Increased supply, rising operating costs, and affordability constraints have impacted occupancy and rent growth in several regions, particularly where development activity has been concentrated.

What drives demand for small-bay industrial?

Demand is driven by local businesses, last-mile logistics, and service providers that require proximity to customers and labor. These uses are less dependent on large-scale economic cycles.

Does multifamily still have a role in portfolios?

Yes. Multifamily remains a core asset class. However, current market conditions have prompted many investors to reevaluate allocation strategies and diversify into other sectors.

Strategic Takeaway

Real estate performance is shaped by more than demand.

It is shaped by supply constraints, tenant structure, and the ability to create value through execution.

Multifamily and small-bay industrial operate under different structural conditions. Understanding those differences is essential when allocating capital in a changing market environment.

Work With Hanson Capital

Hanson Capital specializes in private equity real estate investments focused on high-scarcity industrial assets, disciplined underwriting, and long-term value creation. The firm works with accredited and institutional investors seeking durable income, downside protection, and strategic growth – including 1031 exchange solutions and passive ownership structures.

If you’re curious about how our approach could fit into your portfolio, schedule a call to connect with our team. We’d love to talk through what we’re seeing and where we’re going next.

What We Do

What We Do Our Story

Our Story Core Values

Core Values Meet the Team

Meet the Team Our Approach

Our Approach