When evaluating a real estate investment, most investors immediately look at the projected internal rate of return, or IRR. It has become the headline number in many offering documents and investment summaries.

The problem is that IRR alone rarely tells the full story.

Two investments can produce identical profits but dramatically different IRRs. Conversely, a deal with a strong IRR may generate less total wealth than one with a lower annualized return.

That is why sophisticated real estate investors evaluate IRR and equity multiple together. Each metric answers a different question about how capital performs over time.

Understanding that distinction is essential when evaluating value-add real estate opportunities.

Execution drives returns. Time determines how those returns appear in math.

What IRR Measures in Real Estate

Internal rate of return (IRR) measures the annualized rate of return generated by an investment over time. It accounts for both the magnitude and the timing of cash flows.

In simple terms, IRR answers the question: How quickly is capital compounding each year?

Because IRR is time-sensitive, the timing of distributions has a significant impact on the final number.

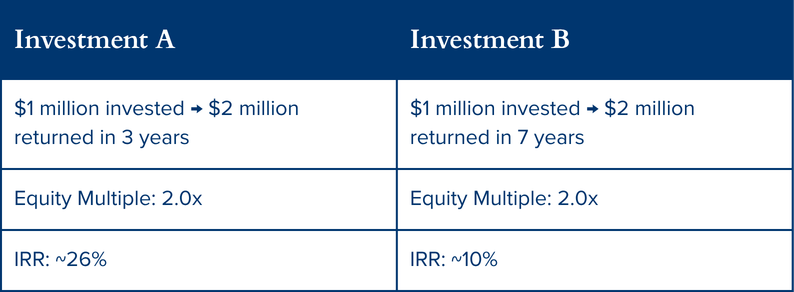

Consider a simplified example:

An investor commits $1 million to a real estate project.

If the investment returns $2 million in three years, the IRR is approximately 26% annually.

If the same $1 million investment returns $2 million in seven years, the IRR falls to approximately 10% annually.

The total profit is identical. The time required to generate it is not.

Speed changes the math.

That is why IRR is often used to evaluate capital velocity. Faster return of capital produces a higher IRR, even if the total profit is unchanged, or, said another way, it allows you to compare returns while accounting for the net present value of cash flows, making it far simpler to compare apples and oranges.

What Equity Multiple Measures

Equity multiple answers a simpler question.

It measures how much total value an investment creates relative to the capital invested.

The formula is straightforward:

Equity Multiple = Total Cash Received ÷ Total Equity Invested

Using the previous example:

- $1 million investment

- $2 million returned

The equity multiple is 2.0x.

Unlike IRR, equity multiple does not account for time. It simply measures the magnitude of the return. Magnitude matters.

If a $1 million investment returns $4 million, the equity multiple is 4.0x regardless of whether the hold period was five years or ten.

This metric is often used to evaluate total wealth creation, not just the speed of returns.

Why Time Changes Everything

Because IRR incorporates timing, small changes in the hold period can dramatically affect the reported return.

For example:

Both deals doubled the investor’s capital. However, the IRR suggests dramatically different performance because capital was returned at different speeds.

This is why evaluating IRR without context can be misleading.

A shorter hold period can produce a strong IRR even if the investment generates modest total profit.

Conversely, longer value creation cycles may produce a lower IRR while generating substantially greater total wealth.

Sophisticated investors evaluate both metrics together.

Why Institutional Investors Look at Both Metrics

Professional real estate investors rarely rely on a single return metric. Instead, they evaluate:

- IRR to understand capital velocity

- Equity multiple to understand magnitude of wealth creation

Each metric provides a different lens on the same investment.

For example, development projects may generate high IRRs if capital is returned quickly after stabilization. However, long-term value-add investments may produce larger equity multiples as operational improvements compound over time.

Both outcomes can be attractive depending on the investment strategy. The key is understanding what drives the numbers.

How These Metrics Appear in Value-Add Industrial Investing

Value-add industrial investments often illustrate the relationship between IRR and equity multiple particularly well.

Operational improvements typically occur over several years. Lease rollovers must occur. Rents must be reset to the market. Physical improvements and tenant repositioning take time.

Value creation is gradual.

However, when those improvements accumulate across multiple assets, the resulting income growth can materially increase asset value at exit.

Hanson Capital’s recent Phoenix industrial portfolio sale offers a clear example.

In February 2026, the firm closed the second and final tranche of an eight-asset portfolio sale to a buyer group backed by J.P. Morgan. Across the second tranche, $9 million of equity capital was converted into $43 million in proceeds.

The transaction produced:

- 4.0x equity multiple

- 35.4% internal rate of return

These results were not the product of rapid capital turnover. They reflected multiple years of operational execution across assets acquired between 2020 and 2021.

Individual properties demonstrated similar dynamics.

A 65,000-square-foot industrial property at 3065 S. 43rd Avenue was acquired in October 2020 for $3.7 million and ultimately sold for $10.5 million, generating a 5.80x equity multiple and 41.55% IRR.

Another property at 4020–4036 S. 15th Avenue, acquired for $2.8 million in January 2020, sold for $8.4 million, producing a 4.88x equity multiple and 41.53% IRR.

In these cases, operational value creation supported both strong equity multiples and strong IRRs. However, the underlying drivers were improvements in leasing, tenant mix, and property positioning rather than short-term market speculation.

Discipline molds value.

Evaluating Real Estate Returns the Right Way

IRR and equity multiple are not competing metrics. They are complementary tools used to understand how an investment performs.

IRR measures the speed of capital growth.

The equity multiple measures the magnitude of capital growth.

Understanding both allows investors to evaluate whether returns are driven by rapid capital turnover, operational value creation, or a combination of the two.

For value-add real estate strategies, especially in supply-constrained industrial markets, returns often emerge through steady operational improvements over time rather than immediate appreciation.

Execution matters more than timing.

Strategic Takeaway

Return metrics only tell part of the story.

Real estate performance ultimately depends on disciplined underwriting, operational execution, and strategic exit timing. IRR and equity multiple help quantify those outcomes, but the underlying drivers remain the same.

Preparation, execution, and discipline matter.

Work With Hanson Capital

Hanson Capital specializes in private equity real estate investments focused on high-scarcity industrial assets, disciplined underwriting, and long-term value creation. The firm works with accredited and institutional investors seeking durable income, downside protection, and strategic growth – including 1031 exchange solutions and passive ownership structures.

If you’re curious about how our approach could fit into your portfolio, visit our website or schedule a call to connect with our team. We’d love to talk through what we’re seeing and where we’re going next.

What We Do

What We Do Our Story

Our Story Core Values

Core Values Meet the Team

Meet the Team Our Approach

Our Approach