What We Do

What We Do Our Story

Our Story Core Values

Core Values Meet the Team

Meet the Team Our Approach

Our Approach

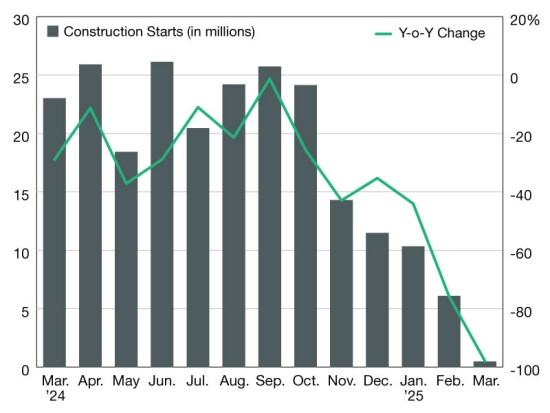

Market Insight #1: Prologis Reports Increased Demand Amid Trade Uncertainty

Prologis, the world’s largest industrial real estate company, anticipates ongoing global trade tensions will drive increased demand for U.S. warehouse space. Companies are strategically stockpiling goods closer to consumers to mitigate tariff-related supply chain disruptions, leading to a surge in leasing activity.

Despite recent slowing of leasing activity and warehouse vacancy rates edging upward to 7% in Q1 2025, Prologis posted strong financial results, including a 9.2% revenue increase to $2.14 billion and net earnings of $592 million. The firm maintains its full-year earnings guidance, predicting further strength as limited warehouse construction constrains new supply and sustains rental rates.

Source:

Market Insight #2: Financial Markets Send Mixed Signals Amid Economic Uncertainty

April 2025 has brought unusual behavior in financial markets, as both stocks and bonds experienced simultaneous gains—a rare occurrence causing concern among analysts about potential synchronized declines ahead. Many attribute this anomaly to erratic U.S. policy shifts and lingering economic uncertainties.

A recent JPMorgan investor survey underscores this uncertainty: 93% expect the S&P 500 to remain at or below 6,000 over the next year, with nearly a third predicting a fall below 5,000. These forecasts represent a stark shift from earlier bullish sentiment, driven by fears of stagflation and unpredictable economic policies.

Sources:

- Financial Times – Stocks and bonds rising together trigger investor anxiety

- Business Insider – Investor sentiment turns cautious as recession concerns rise

Investor Concept of the Week: Capitalizing on Real Estate Resilience Amid Market Uncertainty

The current market presents contrasting signals: industrial real estate continues demonstrating resilience, driven by strategic shifts in global trade and supply chains, while financial markets grapple with volatility and economic uncertainty.

Key Insights:

- Industrial Stability: Prologis’s recent performance highlights ongoing demand strength in strategically positioned warehouse spaces, indicating industrial real estate as a stable asset class amid market turbulence.

- Financial Market Volatility: Investors express caution due to rare simultaneous strength in stocks and bonds, signaling potential for market volatility and uncertainty ahead.

Investor Move:

In volatile market conditions, investors should lean into assets like industrial real estate that show fundamental resilience and steady tenant demand. These uncertain times give us more conviction on why we like multi-tenant diversified cash flow in our investment targets today. Prioritize strategically located, operationally strong industrial properties that can weather short-term economic fluctuations.

Final Thoughts

Despite heightened financial market uncertainties, industrial real estate remains a bright spot, supported by structural trends such as reshoring, e-commerce, and robust logistics demand. Hanson Capital continues to position our portfolio toward these resilient opportunities, aligning our strategies with evolving market conditions to protect and grow investor capital, although with the uncertainty, we’re shifting our risk reward profile towards acquisition over new development.