What We Do

What We Do Our Story

Our Story Core Values

Core Values Meet the Team

Meet the Team Our Approach

Our Approach

FOR IMMEDIATE RELEASE

Contact: Michael Morrison

Hanson Capital Group

406-868-9179

michael@hansonre.com

Hanson Capital Launches Multi-Strategy Real Estate Investment Fund

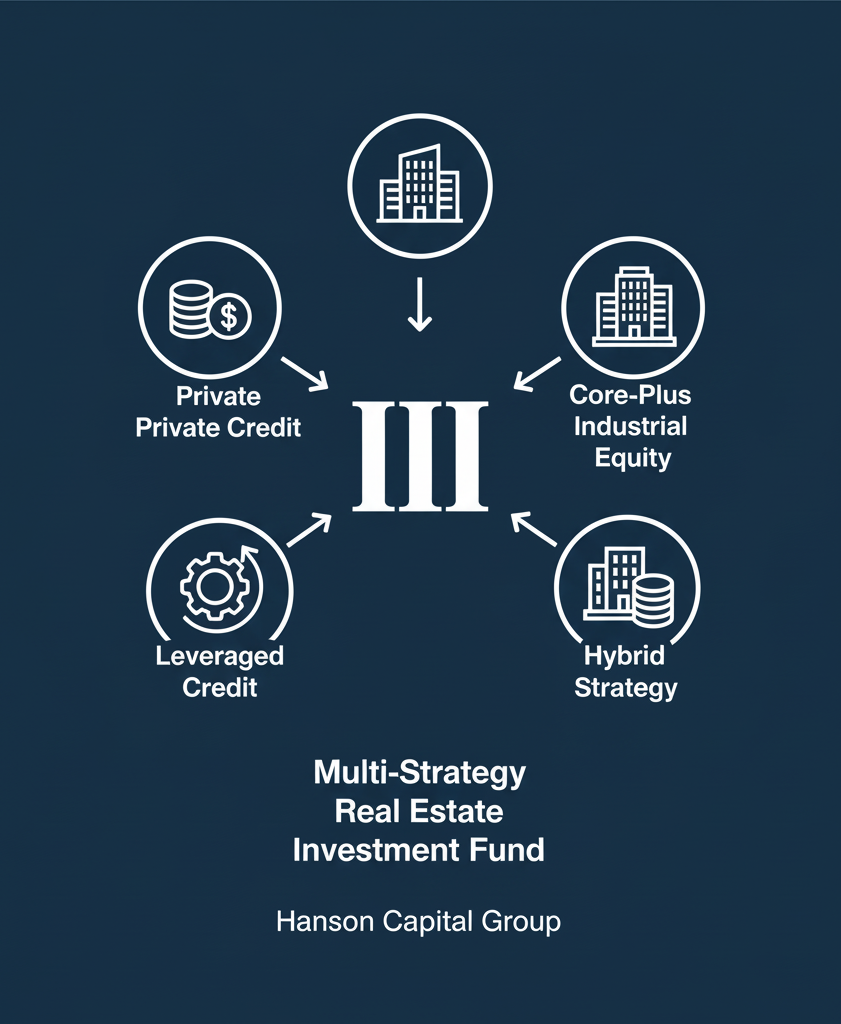

PHOENIX, Dec. 30, 2024 — Hanson Capital Group today announced the launch of Hanson Capital Opportunity Fund III, LLC, an innovative investment vehicle offering four distinct strategies within a single fund structure.

The $250 million fund provides investors the flexibility to participate in any combination of four investment strategies: core-plus equity investments in industrial properties, private credit through real estate-backed lending, leveraged credit investments, and a hybrid approach combining equity, debt, and strategic leverage.

“We’ve structured this fund to give investors precise control over their real estate investment allocation while maintaining the efficiency of a single fund vehicle,” said Chris Hanson, founder and CEO of Hanson Capital Group. “Whether an investor seeks steady income through our lending strategies, long-term appreciation through equity investments, or enhanced returns through our hybrid approach, they can customize their exposure while benefiting from our proven underwriting discipline and risk management.”

The equity strategy targets a 13% IRR through investments in industrial properties, while the private credit strategy aims to deliver 9.5% annual returns. The hybrid strategy, which combines both approaches with strategic leverage, targets a 14.5% IRR.

“Our deep experience in both lending and property acquisition has enabled us to create this innovative structure that addresses diverse investor objectives within a single fund,” said Chris Pike, Principal and Head of Debt at Hanson Capital. “By leveraging our market relationships and proven underwriting processes across multiple strategies, we’re offering institutional-quality investments with the flexibility to match individual investor goals.”

The fund will focus on opportunities throughout the Southwestern United States, where Hanson Capital currently manages $245 million in assets across 1.3 million square feet of commercial property.

About Hanson Capital Group

Founded in 2008, Hanson Capital Group is a vertically integrated real estate investment and lending firm headquartered in Phoenix, Arizona. The firm specializes in acquiring and managing commercial real estate assets and providing real estate-backed lending solutions.