What We Do

What We Do Our Story

Our Story Core Values

Core Values Meet the Team

Meet the Team Our Approach

Our Approach

Most investors focus on purchase price, location, and cap rate when evaluating a real estate investment. Those variables matter. But they are only part of the equation.

The structure of the financing often has just as much influence on the outcome as the asset itself.

Two identical properties can produce very different results depending on how they are financed. The difference is not theoretical. It shows up in cash flow stability, return profile, and exit flexibility.

Financing is not just a way to complete a transaction. It is a strategic lever that shapes both risk and return.

Structure determines outcomes.

What Financing Actually Does in Real Estate

At its core, financing introduces leverage into a transaction.

Leverage amplifies returns by allowing investors to control a larger asset base with less equity. At the same time, it introduces fixed obligations that must be met regardless of performance.

This creates a dual effect:

- It can enhance returns when operations perform as expected

- It can increase risk when performance falls short

Leverage magnifies outcomes in both directions.

Financing also shapes how cash flows behave over time. Debt service requirements influence distributions, and loan terms influence hold strategy. While maturity schedules influence exit timing.

In other words, financing is not separate from the investment. It is embedded within it.

How Debt Influences Returns

The relationship between leverage and returns is often best understood through simple examples.

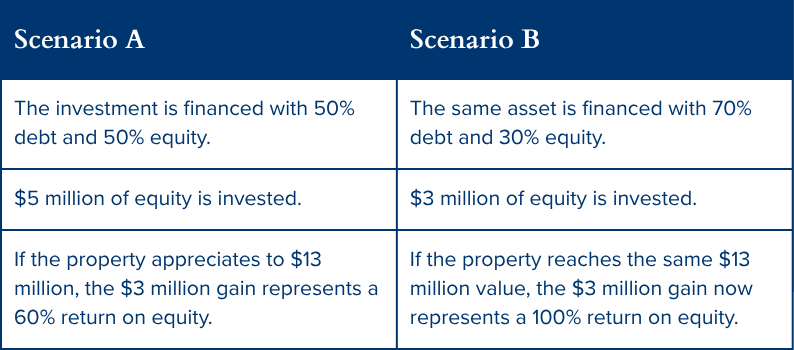

Consider a $10 million industrial acquisition.

Same asset. Same appreciation. Different outcome.

Leverage increases return on equity because less capital is invested upfront. However, this only tells part of the story.

Higher leverage also increases debt service obligations. If income underperforms, cash flow becomes more constrained. That constraint can reduce flexibility and increase risk.

Speed and magnitude diverge.

Higher leverage can improve IRR by reducing initial equity and accelerating capital efficiency. But it can also compress the equity multiple if higher debt service limits distributions over time.

Understanding this balance is critical.

Where Financing Breaks Deals

Financing does not create risk in isolation. It exposes it.

Many real estate investments that appear attractive at acquisition encounter challenges because of how the capital stack was structured.

The most common failure points include:

1. Maturity Mismatch

When loan terms are shorter than the time required to stabilize an asset, investors may be forced to refinance before value creation is complete.

If capital markets tighten at that moment, options become limited.

Timing risk becomes real.

2. Overleverage During Lease-Up

Value-add strategies often rely on increasing occupancy or resetting rents to market rates.

If leverage is too high during this phase, debt service can outpace income. This reduces margin for error and can force suboptimal decisions or additional capital infusions.

Flexibility disappears quickly under pressure.

3. Floating Rate Exposure

Floating rate debt can improve returns in stable or declining rate environments. However, rising rates can materially increase debt service and reduce cash flow.

Without proper hedging or underwriting discipline, interest rate volatility can erode projected returns.

Debt structure matters as much as asset quality.

Financing Strategy in Value-Add Industrial

In value-add industrial investments, financing must align with the operational business plan.

Lease rollover, tenant improvements, and rent resets take time. Income does not increase immediately. It improves gradually as leases turn and market rents are captured.

Financing must accommodate that timeline.

If loan maturities are too short, or if debt service requirements are too aggressive, the investment may be forced into a refinance or sale before stabilization is achieved.

That outcome is avoidable with disciplined structuring.

For example, aligning loan terms with expected lease rollover cycles allows income to stabilize before refinancing. Structuring debt with appropriate coverage ratios provides flexibility during transitional periods.

This is where capital structure becomes strategic rather than mechanical.

Execution requires time. Financing must allow for it.

How Sophisticated Investors Approach Debt

Institutional investors do not evaluate financing solely based on interest rate or leverage level. They evaluate how well the capital structure supports the business plan.

The framework is straightforward:

1. Match Debt to Strategy

Stabilized assets may support higher leverage and tighter loan terms. Transitional assets require more flexibility.

2. Preserve Optionality

Financing should create options, not eliminate them. Longer maturities, extension options, and conservative leverage can provide flexibility in uncertain environments.

3. Underwrite Downside First

Rather than optimizing for maximum leverage, disciplined investors evaluate how a deal performs under stress scenarios.

What happens if rents grow slower than expected?

What happens if interest rates increase?

What happens if leasing takes longer?

Downside protection is engineered.

4. Avoid Forced Decisions

The goal is to avoid situations where external factors dictate outcomes. Financing should allow investors to choose when to refinance or sell, not be required to act.

Control matters.

The Role of Financing in Institutional Outcomes

Well-structured financing does not guarantee success. But poorly structured financing can undermine even strong assets.

In Hanson Capital’s experience, capital structure is one of the most consistent drivers of both performance and risk mitigation.

The firm’s perspective is informed by experience across both debt and equity. This provides visibility into how financing decisions affect asset-level performance over time.

That visibility reinforces a core principle: Financing should support execution, not constrain it.

Evaluating Financing Beyond the Interest Rate

The interest rate is often the most visible component of a loan. It is also one of the least complete measures of financing quality.

More important considerations include:

- Loan term relative to business plan

- Debt service coverage during transitional periods

- Flexibility through extension options

- Exposure to rate volatility

- Alignment with exit strategy

- These variables determine whether financing enhances or limits investment outcomes.

Details matter.

Strategic Takeaway

Financing is not a secondary consideration in real estate investing. It is a central component of how outcomes are shaped.

The right capital structure enhances flexibility, supports execution, and protects against downside risk. The wrong structure can limit options and introduce avoidable pressure.

Returns are influenced by markets.

They are determined by execution.

They are shaped by structure.

Work With Hanson Capital

Hanson Capital specializes in private equity real estate investments focused on high-scarcity industrial assets, disciplined underwriting, and long-term value creation. The firm works with accredited and institutional investors seeking durable income, downside protection, and strategic growth – including 1031 exchange solutions and passive ownership structures.

If you’re curious about how our approach could fit into your portfolio, visit our website or schedule a call to connect with our team. We’d love to talk through what we’re seeing and where we’re going next.